Country risk

Rabobank Risk Rating: Breakdown of corporate loans

56 Rabobank Group Annual Report 2004

Organisation and risk management

An important element in the process of approving financing applications

is the assigning of a rating that indicates the likelihood of a client being

unable to repay the loan. This likelihood is referred to as the probability

of default (PD). In 2003, Rabobank Group introduced the Rabobank Risk

Rating (RRR), which reflects the counterparty's probability of default over

a one-year period and which is applied to all larger corporate clients.

The system comprises 25 ratings. Ratings R0 to R20 imply that financing

commitments are met. R0 means the absence of risk and R20 means

that the financial position is considered very weak. Ratings D1 to D4

indicate in principle that payment commitments are no longer being

met and that the collectibility of the loan is doubtful. D4 stands for

bankruptcy or a comparable situation.

The portfolio's average rating is between R11 and R14. For 2% of the

portfolio, the commitments are not being fully met and an adequate

provision has been formed for this part of the portfolio. It should be

noted that the breakdown indicates only the extent to which Rabobank

expects that clients can or cannot meet their commitments. In many

cases, the bank has obtained adequate security that can be invoked

should the client no longer meet its financing commitments, ensuring

that the loan is eventually fully or partly repaid. Accordingly, Rabobank

Group has a healthy corporate loan portfolio. This healthy condition

applies even more so to the total loan portfolio, half of which consists of

residential mortgages, where the risk of losses is historically very low.

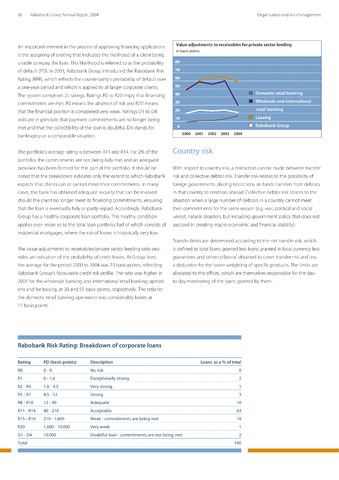

The value adjustments to receivables/private sector lending ratio pro

vides an indication of the probability of credit losses. At Group level,

the average for the period 2000 to 2004 was 23 basis points, reflecting

Rabobank Group's favourable credit risk profile. The ratio was higher in

2004 for the wholesale banking and international retail banking operati

ons and for leasing, at 30 and 59 basis points, respectively. The ratio for

the domestic retail banking operations was considerably lower, at

17 basis points.

Value adjustments to receivables for private sector lending

in basis points

80

70

60

50

40

Domestic retail banking

30

Wholesale and international

retail banking

10

Leasing

0

HI Rabobank Group

2000 2001

2002 2003 2004

With respect to country risk, a distinction can be made between transfer

risk and collective debtor risk. Transfer risk relates to the possibility of

foreign governments placing restrictions on funds transfers from debtors

in that country to creditors abroad. Collective debtor risk relates to the

situation when a large number of debtors in a country cannot meet

their commitments for the same reason (e.g. war, political and social

unrest, natural disasters, but including government policy that does not

succeed in creating macro-economic and financial stability).

Transfer limits are determined according to the net transfer risk, which

is defined as total loans granted less loans granted in local currency less

guarantees and other collateral obtained to cover transfer risk and less

a deduction for the lower weighting of specific products. The limits are

allocated to the offices, which are themselves responsible for the day-

to-day monitoring of the loans granted by them.

Rating

PD (basis points)

Description

Loans as a of total

R0

0-0

No risk

0

R1

0-1.6

Exceptionally strong

2

R2-R4

1.6-4.5

Very strong

1

R5-R7

4.5-12

Strong

3

R8- R10

12-40

Adequate

10

R11 -R14

40-210

Acceptable

63

R15-R19

210-1,600

Weak - commitments are being met

18

R20

1,600- 10,000

Very weak

1

D1 -D4

10,000

Doubtful loan - commitments are not being met

2

Total

100